|

|

|

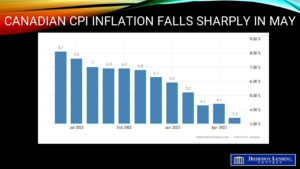

Grocery prices remain elevated–up 9.0% y/y–down only one tick from April. Prices for food purchased from restaurants rose slightly faster year-over-year in May (+6.8%) than in April (+6.4%), amid ongoing elevated labour shortages, input costs and expenses, which Stats Can data show job vacancies can disproportionately affect these businesses.

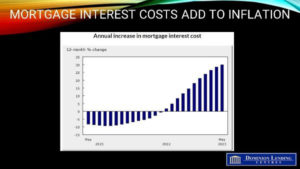

Rising interest rates also boost inflation. This is because mortgage costs are just over 3% of the CPI. They are a part of the most significant component of the index–shelter–which represents almost 30% of the index. The mortgage interest cost index rose by a whopping 29.9% in May, following a 28.5% increase in April. This was the largest increase on record for the third consecutive month, as Canadians continued to renew and initiate mortgages at higher interest rates. And, of course, this does not include the effects of the policy rate hike in June.

It takes time for the full effect of interest rate hikes entirely feed into the CPI. Mortgage interest costs will continue to rise as higher interest rates flow gradually through to household mortgage payments with a lag as contracts are renewed. And home-buying related expenses ticked higher in May, with higher home resale prices increasing realtor and broker commissions.

|

Please Note: The source of this article is from SherryCooper.com/category/articles/